By Robert A. Peterson, PhD

Introduction

Direct selling is a business model that offers entrepreneurial opportunities to individuals who, as independent contractors, market products and services to consumers, typically outside of a fixed retail establishment through one-to-one selling, in-home product demonstrations, or online. Direct sellers have job titles such as distributor, representative, consultant, associate, or brand partner. They may participate in direct selling in various ways, including selling products and services themselves or through their sales organizations, providing training and leadership to their sales organizations, referring customers to their company, and purchasing products and services for personal use. Compensation is ultimately based on sales and may be earned through personal sales and/or the sales of others in their sales organization.

In 2024, direct selling generated $34.7 billion in retail sales in the United States and involved an estimated 5.4 million individuals who were actively engaged in building their own direct selling businesses.

Despite its ubiquity and contribution to the economy, the full economic impact of direct selling in the United States is often understated. Therefore, the purpose of the present analysis was to estimate the economic impact of direct selling activity in 2024 through the application of an input-output economic model. Given the retail sales generated by direct selling (i.e., its Direct Effect), the model (implemented by means of IMPLAN® software and data) estimated the

- Indirect Effect (upstream or supply chain sales) due to direct selling and

- Induced Effect (downstream sales due to household spending) associated with the Direct and Indirect Effects.

Collectively, these three effects—Direct, Indirect, and Induced—represent the economic impact of direct selling activity on the nation’s economy. In addition, the analysis estimated the fiscal (tax) implications of direct selling activity in the United States.

Executive Summary

An input-output economic modeling of 2024 direct selling sales activity was undertaken using IMPLAN® software and data obtained from the federal government[1]. Direct selling (retail) sales data were provided by the Direct Selling Education Foundation (DSEF). The purpose of the modeling was to estimate the economic impact of direct selling activity in the United States in 2024.

Results are reported in terms of Direct, Indirect, and Induced Effects using a measure of gross economic output, sales dollars. Gross economic output refers to the cumulative value of production. Unlike Gross Domestic Product (GDP), gross economic output includes intermediate goods and services. (GDP is synonymous with total output less intermediate inputs.)

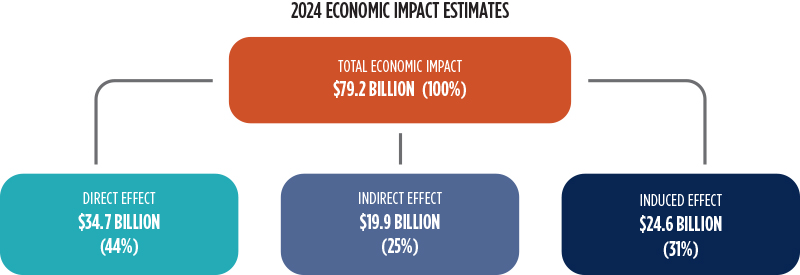

Using the DSEF estimate of $34.7 billion in direct selling (retail) sales in 2024 as a starting point, the total economic impact of direct selling activity in the United States in 2024 was estimated to be $79.2 billion. The $79.2 billion economic impact consisted of

- The Direct Effect of direct selling, $34.7 billion

- The Indirect (upstream or supply chain) Effect of direct selling, $19.9 billion, and

- The Induced (downstream or household) Effect of direct selling, $24.6 billion.

Because of (1) the modeling approach and (2) the nature of the industry (e.g., the widespread use of independent contractors), the total estimated economic impact of $79.2 billion should be considered conservative.

The derived multiplier emanating from IMPLAN® modeling was 2.28. This multiplier means that nationally $1.00 in direct selling (retail) sales produced an economic impact of $2.28 in 2024.

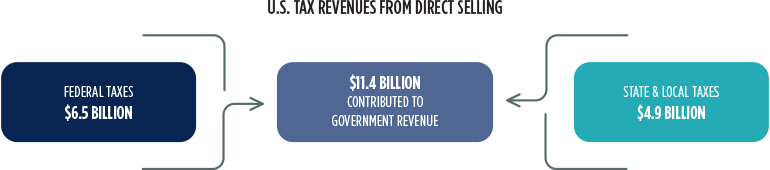

In 2024, the economic impact of direct selling activity produced an estimated $6.5 billion in federal taxes and $4.9 billion in state and local taxes, or $11.4 billion in total taxes. The total value of direct selling activity (i.e., the Direct, Indirect, and Induced Effects) added to the nation’s Gross Domestic Product in 2024 was estimated to be $79.2 billion.

Overview and Methodology

The present modeling estimated the economic impact of direct selling activity in the United States in 2024 using the IMPLAN® input-output economic model. Specifically, in the present context, gross economic activity refers to sales dollars generated and distributed throughout the United States economy. The sources of activities that sum to economic output consist of both capital expenditures and operating expenditures, including spending on goods and services by direct selling firms, the Direct Effect, as well as by firms within the direct selling supply chain, which leads to the Indirect Effect, and off-site spending on goods and services by households in which a member earns income from a direct selling company or supply chain company, the Induced Effect.

A series of multipliers link Direct, Indirect, and Induced Effects. These multipliers are based on data compiled by several federal entities and include the Bureau of Economic Analysis Benchmark Input-Output Tables. (See Appendix for details.) A summary metric, the derived or implied direct selling multiplier, estimates the impact of one direct selling sales (retail) dollar on gross economic output due to inter-industry and industry-employee household relationships between the direct selling industry and other industries.

Conceptually, the multipliers quantify the economic ripple effect of inter-industry economic activity. This ripple effect can be positive or negative depending on whether a modeled entity is expanding or contracting. Multipliers are static and do not account for disruptive shifts in infrastructure without specifically addressing infrastructure changes. The present model applies the most current (2024) IMPLAN® multipliers.

Data

DSEF conducts an annual “Growth & Outlook” market-sizing survey to estimate the size and scope of the direct selling industry in the United States. It engages Cadmus, an international consulting firm, to conduct this survey, perform secondary research, and generate industry-wide estimates.

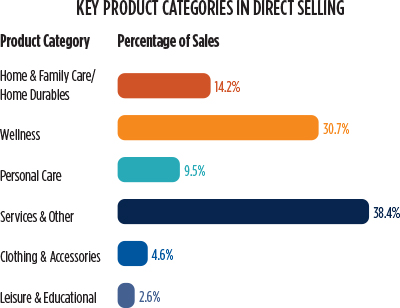

Cadmus market-sizing estimates are reviewed and further refined by DSEF. Results that are reported include total direct selling (retail) sales as well as (retail) sales estimates by selected geographical regions, by compensation structure of direct selling firms, by sales strategy, and by major product categories. The six product categories utilized in the present analysis are:[2]

- Wellness—Weight management products and programs, nutritional supplements, sports/energy and body-building, health foods and beverages, children’s supplements, health/nutrition/fitness instructional materials, and essential oils and pharmacy.

- Services—Financial services, telecommunications, internet services, energy, legal services, group buying, and travel services.

- Home and Family Care and Home Durables—Home and auto care cleaning products, and food and beverages (excluding those in the wellness category). Home durables includes cookware, cutlery, house/kitchenware, various home gifts, and home appliances.

- Personal Care—Cosmetics, skin care, fragrances, hair and nail care, and various toiletry products.

- Clothing and Accessories—Clothing, lingerie, sleepwear, shoes, jewelry, and fashion accessories.

- Leisure and Educational—Books, encyclopedias, educational publications, computer software, crafts, and toys and games.

The DSEF’s 2025 Growth & Outlook Report (retail) sales estimate formed the basis of IMPLAN® modeling. Specifically, according to the DSEF, direct selling (retail) sales totaled $34.7 billion in 2024. The $34.7 billion in direct selling (retail) sales was initially modeled in IMPLAN® with margins applied. This was equivalent to identifying the economic impact of operating a business with $34.7 billion in retail sales. It excluded the manufacturing, wholesaling, and transporting of goods, and included only the economic activities associated with direct selling companies.

Wholesaling and manufacturing Indirect Effects of direct selling activity due to the industry supply chain were sequentially modeled by respectively applying margins to direct selling (retail) sales activity and wholesale sales activity. For wholesaling, this allowed the identification of the economic effects of operating the equivalent of a wholesale business. The wholesale industry modeling included transportation but excluded the effect and supply chain of the manufacturing component.

Manufacturing activity was estimated after applying margins to and subtracting direct selling economic activity and wholesaling economic activity. Manufacturing sales activity was modeled using the six product groups (e.g., wellness, personal care, etc.) above.

The Induced Effect of direct selling activity was estimated for each sector modeled (i.e., retailing, wholesaling, and manufacturing) and aggregated to reflect its total estimated economic impact.

Taxes attributable to direct selling activity were also estimated using the IMPLAN® model. The tax estimates provided in this report include tax revenue derived from direct, indirect, and induced sales activity. The national economic impact tax estimate includes both federal taxes and state/local taxes.

Economic Impact

The $34.7 billion in direct selling (retail) sales nationally contributed a total economic impact of $79.2 billion to the national economy in 2024 through its combined indirect and induced effects. As shown above, the 2024 national economic impact included $34.7 billion in direct selling sales activity, $19.9 billion in indirect sales activity, and $24.6 billion in induced sales activity.

The derived (implied) multiplier resulting from IMPLAN® modeling summarizes the economic impact of one direct selling (retail) sales dollar ($1) on the national economy. It is calculated as the total economic impact divided by the direct effect (i.e., $79.2B/$34.7B = 2.28 in 2024). Thus, for example, $1 in direct selling sales (the direct effect) generated a total economic impact of $2.28 in 2024. The derived multiplier in 2024 is somewhat smaller than derived multipliers observed in other retailing sectors (approximately 2.44 on average).

Fiscal Impact

Tax impacts estimated by IMPLAN® are respectively categorized as federal taxes and state and local taxes. IMPLAN® quantifies tax impacts based on employee compensation, proprietor income, and taxes on production and imports, households, and corporations. Estimated taxes range from federal and state income taxes and property taxes to sales taxes and motor vehicle licenses. As such, the estimated total (direct, indirect, and induced) federal, state, and local tax revenues attributable to direct selling activity in the United States in 2024 were $11.4 billion. Federal tax revenues attributable to the $34.7 billion in direct selling activity were estimated at $6.5 billion in 2024. State and local taxes attributable to direct selling activity were estimated at $4.9 billion in 2024.

About IMPLAN®

IMPLAN® is an input-output economic model based on aggregating and connecting a multitude of economic databases, foremost of which are the Bureau of Economic Analysis (United States Department of Commerce) Benchmark Input-Output Tables.[3] It consists of both software and data that together permit detailed estimates of various economic impacts. The IMPLAN® model quantifies inter-industry relationships within an economy by documenting how the output of one industry becomes the input of another industry. Through a backward-linking process, the present modeling captured the relationship between economic activity in the direct selling industry and economic activity in its (general) supply chain (i.e., the Indirect Effect of direct selling activity on the wholesaling and manufacturing firms in the direct selling industry supply chain) as well as the ancillary (household) effect that direct selling activity has on the economy (i.e., the Induced Effect).

The primary databases contained and used in IMPLAN® modeling are respectively compiled and updated by the United States Census Bureau, the United States Bureau of Economic Analysis, the United States Department of Agriculture, and the United States Bureau of Labor Statistics.

Numerous multipliers were used in the present analysis to link the six (aggregated) product categories and the manufacturing sector (which were in turn linked to the wholesale and retail sectors). In particular, product subcategories were matched with 6-digit NAICS codes which were in turn linked to their respective 528 IMPLAN® sectors. Because the Nonstore Retailers Sector encompasses more establishments than those traditionally defined as direct selling companies, its associated multiplier might be somewhat attenuated. However, any possible attenuation was not believed to substantially affect the results of the estimation process or the final economic impact estimation due to limiting the modeling to particular product categories.

Specifically, when modeling the manufacturing sector, the multipliers associated with the six direct selling product categories incorporated the categories’ relative sales and the percentage of category manufacturer sales that originated in the United States (based on federal data sources). The 2024 direct selling (retail) sales percentages were based on the DSEF’s 2025 Growth & Outlook Report estimates, whereas the 2024 domestic purchasing percentages (related to local purchasing coefficients in IMPLAN®) were based on 2023 federal statistics.

Within the six product categories, subcategories were aggregated to form each respective product category. For instance, as previously shown, two IMPLAN® subcategories (Clothing, Lingerie, Sleepwear and Shoes, and Jewelry and Fashion Accessories) were aggregated to create the Clothing & Accessories product category. Trade flows and industry data for the subcategories were combined in IMPLAN®, and multipliers were generated by IMPLAN® software. (Note: the combination was not a simple average.) To the extent that product category data do not comport exactly with direct selling product offerings or sales, the multipliers might be somewhat attenuated. However, the consequence of such potential attenuation was not deemed substantial.

The overall derived multiplier, 2.28, was composed of the Direct Effect implied multiplier 1.00, the Indirect Effect implied multiplier .57, and the Induced Effect implied multiplier .71.

Where appropriate, default values of the IMPLAN® software were applied during modeling. Consequently, all estimated values—multipliers as well as effects and impacts—should be considered conservative.

[1] IMPLAN® is widely used in industry and government analyses. See www.implan.com

[2] The product categories include, but are not limited to, the illustrative subcategories.

[3] Frances Day, “Principles of Impact Analysis & IMPLAN® Applications.” IMPLAN® stands for IMpact Analysis for PLANning.

Dr. Robert Peterson is Professor Emeritus of Marketing and John T. Stuart III Centennial Chair of Marketing (Emeritus) at The University of Texas.

References

- Direct Selling Education Foundation. 2025 Growth & Outlook Report.

- IMPLAN Group, LLC. IMPLAN® 2023. Huntersville, NC. IMPLAN.com.

- Robert A. Peterson. The Economic Impact of Direct Selling Activity in the United States in 2016.

- Robert A. Peterson. The Economic Impact of Direct Selling Activity in the United States in 2022.

- United States Bureau of Economic Analysis. Real Gross Domestic Product, Chained Dollars, bea.gov.

- United States Bureau of Economic Analysis. Personal Income and Its Disposition, Monthly, bea.gov.

- United States Census Bureau. Retail and Food Services Sales, census.gov.

- United States Census Bureau. Nonemployer Statistics by Legal Form of Organization and Receipts Size Class for the United States, States, and Selected Geographies, census.gov.

Acknowledgment

Appreciation is expressed to the Business Research Division, Leeds School of Business, University of Colorado, Boulder, for its analytical support.

Direct selling is a business model that offers entrepreneurial opportunities to individuals who, as independent contractors, market products and services to consumers, typically outside of a fixed retail establishment through one-to-one selling, in-home product demonstrations, or online. Direct sellers are called distributors, representatives, consultants, associates, or various other titles. They may participate in direct selling in various ways, including selling products and services themselves or through their sales organizations, providing training and leadership to their sales organizations, referring customers to their company, and purchasing products and services for personal use. Compensation is ultimately based on sales and may be earned through personal sales and/or the sales of others in their sales organization.

Direct selling is a business model that offers entrepreneurial opportunities to individuals who, as independent contractors, market products and services to consumers, typically outside of a fixed retail establishment through one-to-one selling, in-home product demonstrations, or online. Direct sellers are called distributors, representatives, consultants, associates, or various other titles. They may participate in direct selling in various ways, including selling products and services themselves or through their sales organizations, providing training and leadership to their sales organizations, referring customers to their company, and purchasing products and services for personal use. Compensation is ultimately based on sales and may be earned through personal sales and/or the sales of others in their sales organization. These three effects—Direct, Indirect, and Induced—collectively represent the economic impact of direct selling activity on the nation’s economy. In addition, the analysis estimated the fiscal (tax) implications of direct selling activity in the United States.

These three effects—Direct, Indirect, and Induced—collectively represent the economic impact of direct selling activity on the nation’s economy. In addition, the analysis estimated the fiscal (tax) implications of direct selling activity in the United States. Because of (1) the analytic approach and (2) the nature of the industry (i.e., the widespread use of independent contractors), the total estimated economic impact of $111.4 billion should be considered conservative.

Because of (1) the analytic approach and (2) the nature of the industry (i.e., the widespread use of independent contractors), the total estimated economic impact of $111.4 billion should be considered conservative.