How digitally native entrepreneurs are turning the USD 400 billion wellness direct-selling sector into a new pathway to economic independence.

Read more at entrepreneur.com here.

How digitally native entrepreneurs are turning the USD 400 billion wellness direct-selling sector into a new pathway to economic independence.

Read more at entrepreneur.com here.

Dr. Manfred Krafft, Professor of Marketing at the University of Muenster and DSEF Fellow, goes over the various motivations people have for involving themselves in direct selling businesses.

DSEF Fellow Dr. Sandy Jap, The Sarah Beth Brown Endowed Professor of Marketing at Emory University, explains the priorities of direct sellers beyond the desire for independence and flexibility.

By Caroline Glackin, PhD and Murat Adivar, PhD

The study applies predictive analytics to data from the 2018 National Salesforce Survey commissioned by the Direct Selling Association. It identifies key factors in salesforce motivation and performance theories studied within Expectancy Theory (Vroom 1964), Herzberg’s (1959) Two Factor Theory, and the job demands and resources model (JD-R) (Bakker and Demerouti 2007). Academic researchers dedicate substantial efforts to studying salesforce motivation and performance, but the power of machine learning has not been applied to direct sellers as independent representatives until now.

By employing supervised learning algorithms for predictive analytics to create models for (1) recruits and (2) existing independent representatives, the study finds that the most crucial factors align with Vroom’s Expectancy Theory (1964), which posits that motivation is influenced by the belief that effort will lead to desired outcomes. For recruits, the key predictors of selling success include allocated time for direct selling, ability to find new customers, gender, and adopting direct selling as a career. Time invested, experience of direct selling, recruitment, tenure, and use of technology are most predictive for top-producing direct sellers. Direct Selling Organizations (DSO) can customize their recruitment, training, and incentives to maximize sales performance by having such analysis for their organizations. This work has the potential to improve the landscape for recruitment, retention, and success.

DSOs foster an entrepreneurial culture and mindset through entrepreneurial training, tools, and professional networking (Peterson and Wotruba 1996). Crittenden, Crittenden, and Ajjan (2019) state, “Independent distributors are backed by established brands who provide them…quality products, marketing tools, business education, and a wealth of digital resources for professional and personal development.”

Representatives are DSOs’ go-to-market strategy and channel, and revenues depend on successful recruitment, retention, and performance. Because no sales experience is required and recruitment occurs primarily through an independent contractor salesforce, successful selection is essential. With a low entry cost for starter kits (average of $199 per Gamse, 2016), training, mentoring, and performance incentives matter.

DSOs focus on fostering entrepreneurial cultures and offering transparency in the company-distributor-customer dynamic (Fleming 2017). Traditional attitudinal variables like organizational commitment, expectations, satisfaction, and motivation matter (Kim and Machanda 2021). Non-pecuniary benefits, income, personal networks, and autonomy and others influence sellers (Coughlan et al. 2016, Wotruba and Tyagi 1992). These add to the broader sales performance literature.

DSOs have unique brands and cultures, which they share with sellers. This collaborative culture supports networks and promotes teamwork, coaching, and mentoring, rather than fostering competitive sales environments (Bhattacharya and Mehta 2000; Biggart 1989; Crittenden and Crittenden 2004; Lan 2016; Merrilees and Miller 1999). Representatives’ lives are intertwined with the brand and company, finding more than just a job but a community and worldview (Biggart, 1989). They often join for the products and stay for the supportive environment (Coughlan et al. 2016). Research suggests that meeting realistic expectations is more important than overselling for job satisfaction (Wotruba and Tyagi 1992).

The factors identified are like those for salesforces and entrepreneurs. This is logical, considering that direct selling representatives operate as self-employed micro-entrepreneurs with intricately linked relationships to their direct selling companies.

The underlying theoretical frameworks on needs, motivations, and expectations in the literature suggest determinants to examine. While machine learning remains agnostic to theory, classic research continues to add value to the discussion and is incorporated into the framework.

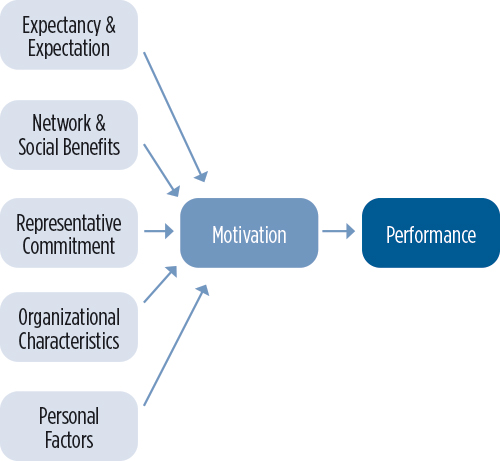

We developed a taxonomy to identify key factors influencing direct selling representative performance, such as education, tenure, and experience. Without forming specific hypotheses, our evidence-driven approach highlights determinants like expectations, social benefits, commitment, organizational traits, and personal factors that impact salesforce motivation and performance. See Figure 1 for details.

Figure 1

Salesforce Performance Determinants from the Literature

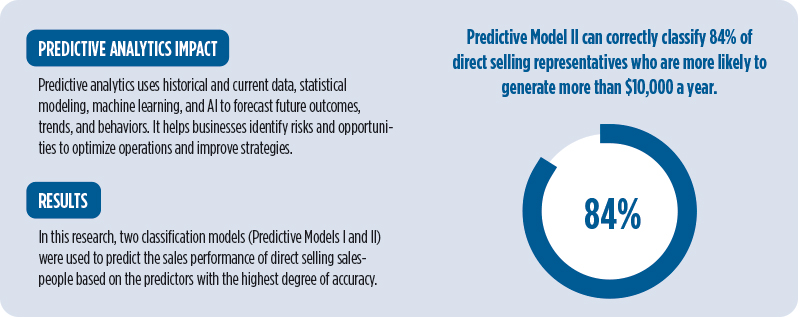

We created two classification models (Model I and Model II) to predict the sales performance of direct selling salespeople based on the predictors with the highest degree of accuracy (see also Glackin and Adivar 2023). Sales performance is assessed by the salesperson’s reported annual direct selling business net income.

A supervised learning approach in which the outcome is the independent sales representative’s financial performance, dependent on some direct seller-specific inputs is the least biased, strongest method available (Glackin and Adivar 2023; Habel et al. 2024). To attain the goal using supervised learning, we employ the 2018 DSA Salesforce Survey dataset of 6,941 direct selling representatives, including a range of personal factors, experiences, attitudes, and interests. DSOs among the 122 members of the Direct Selling Association distributed the survey. The survey queries on the respondent’s gender, desire to dedicate time to direct selling, capacity to find new clients, motives to become and remain representatives, and numerous other topics. The sample for this study is a subset of the entire dataset of 8,714 entries to incorporate active sales representatives who answered the question regarding net income from direct selling and did not respond “don’t know.”

The survey question regarding net income from direct selling is crucial, as it is used to gauge the direct seller’s financial success (performance) of direct sellers. This question in the survey could be answered with one of 15 income levels between $0 and $400,000. Our exploratory analysis indicates that DSOs should identify the characteristics of direct sellers who earn more than $10,000 annually in net income, which results from data clustering and as the accepted norm for “business builders” in direct selling. Even though this is a modest annual net income for a salesperson, it is a crucial level of productivity for the channel. The direct selling channel generated more than $30 billion in annual revenue, according to an approximate extrapolation of industry sales statistics predicting $40.1 billion in revenue in 2020 from the DSA 2021 Growth and Outlook Report. We construct our target response (“Above$10,000”) as a binary variable by combining 15 levels of the categorical variable.

Utilizing domain expertise and current literature, we tested variables that are readily available to DSOs and can predict the financial success of independent salesforces before and after recruitment. Using the variable selection and dimension reduction tools of our data analytics platform, we excluded the tested predictors that had no measured effect on the models’ precision. We combined the recorded states of the dependent variable into two levels as another dimension reduction strategy. Using best practices, we divided the dataset into training and validation sets, compared machine learning methods on the validation set, and raised the target-level accuracy of the selected classification algorithm by adjusting the classification probability threshold.

In this study, we utilize supervised learning to predict high-performing independent sales representatives before and after recruitment. Our supervised learning task is building classification models that predict the class of categorical responses. The data analysis platform is JMP Pro (by SAS) and requires the selection of suitable machine learning algorithms for classification. We employ the following classification techniques and evaluate probable independent variables to build two classification models: Decision Trees, Boosted Tree, Bootstrap Forest, Logistic Regression, and K-Nearest Neighbors. For superior performance in models, the independent variables with the strongest predictive contribution are employed as predictor variables.

Model I – Classification Model for Recruits

We used multiple supervised learning approaches (i.e., Decision Trees, Logistic Regression, Naive Bayes, K-Nearest Neighbors, and Bootstrap Forest) to identify the optimal model for predicting the success of an applicant based on data knowable at recruitment. We explored 16 independent and 14 underlying variables for model building. Model I intended to predict the direct seller recruits that were most likely to earn an annual net income of more than $10,000 from their efforts. Decision (classification) Trees with a particular profit matrix (connected with the goal response) produced the highest classification accuracy. In this study, 78% of validation data at the target level “Above10K=1” were correctly categorized by Model I with the set probability threshold value of 0.21.

These values can be interpreted as follows: In a scenario where a DSO employs this classification model to choose the top 20% of new representatives expected to net more than $10,000 annually from direct selling, the organization will receive 2.5 more target-level applicants than with “no model baseline.”

Table 1

Model I – Recruitment

| Variable | Survey Question/Predetermined Response | Number of Splits | G^2(*) | Portion |

|---|---|---|---|---|

| HOURS_DS | How many hours per week do/did you spend on your direct selling business? | 6 | 789.1447 | 0.6744 |

| ATTEMPT_SELL | In a typical month, how many new potential customers do you attempt to sell to? | 9 | 153.5405 | 0.1312 |

| CAREER | Direct selling is a career for me | 6 | 71.2069 | 0.0609 |

| GENDER | Please indicate your gender | 6 | S1.2537 | 0.0438 |

| DISCOUNT | I get the products at a discount | 6 | 37.5171 | 0.0321 |

| SOCIAL | To meet new people/expand my social circle | 4 | 35.9346 | 0.0307 |

| SUPP_INC | Long-term supplemental income | 9 | 31.487 | 0.0269 |

*In the report, G2 (likelihood-ratio chi-square) is twice the [natural log] entropy or twice the change in entropy. In classification trees, the largest G2 value is the dividing criteria. The portion column indicates die percentage of G2 or the sum of squares attributable to the variable (i.e.. portion column shows the contribution of the variable to the model)

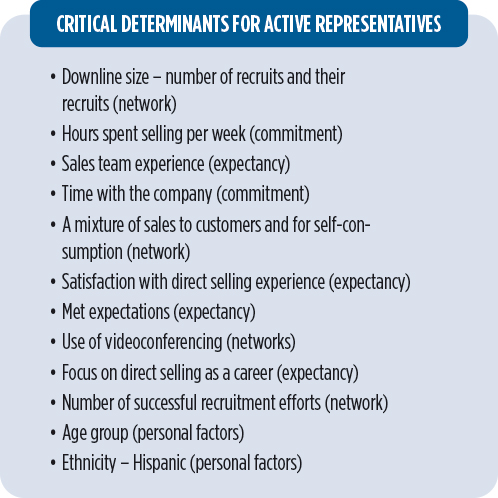

Model II: Classification Model – Active Sales Representatives

In this part, we create a prediction model and identify the most relevant elements influencing the financial performance of current (active) direct salespeople utilizing determinants that are only available once a representative is an active independent representative. This model included 35 independent variables with their comprehensive underlying variables.

The outputs are described in Table 2.

Table 2

Model II – Active Sales Representatives

| Variable | Survey Question/Predetermined Response | Number of Splits | G^2(*) | Portion (* *) |

|---|---|---|---|---|

| DOWNLIINE | q55: What is the total number of independent representatives in your downline? | 2214 | 391.8158 | 0.2493 |

| HOURS_DS | q13: how many hours per week do/did you spend on your direct selling business? | 1504 | 216.9524 | 0.1380 |

| SALESQUAL | q14r4: I have developed a sales team of my own – Please answer the questions below based on your current direct selling experience. | 546 | 176.9932 | 0.1126 |

| TENURE | q19: How long have you represented your company? | 2029 | 130.2316 | 0.0828 |

| SALESTYPE | q38r1: Sales to your customers- Of all the orders you place per month, what percentage are: | 1952 | 128.7537 | 0.0819 |

| SATIS_DS | q2I: How do you rate your actual experience in direct selling? Has it been…? | 1389 | 124.1606 | 0.0790 |

| MET_EXPECT | q20: Now, please think about your expectations when you started direct selling. Has your experience… | 1116 | 90.3898 | 0.0575 |

| VIDEOCONF | q65r5: I use Zoom, Skype, Google Hangouts (or other video conferencing) for business | 1184 | 69.4189 | 0.0442 |

| CAREER | q23r1c2: Direct selling is a career for me | 1072 | 67,2371 | 0.0428 |

| INC_SATIS | q78: How satisfied are you with the amount of money earned for the amount of time you spend on your direct selling business? | 1303 | 62.7765 | 0.0399 |

| SUCCESS_RCRT | q52: In a typical month, how many people do you SUCCESSFULLY recruit? | 958 | 45.0898 | 0.0287 |

| AGE_GR | Age Group | 1550 | 39.6218 | 0.0252 |

| LATINX | q16 (Ethnicity): Are you of Hispanic or Latino origin? | 858 | 28.5079 | 0.0181 |

(* *) Portion column shows the contribution of the variable to the model

The indication column “Above10K” is the response to which our analysis is directed. The estimation of the model’s accuracy is based on the misclassification rate across the validation set. Bootstrap Forest and Boosted Tree outperform other supervised learning algorithms with an 88% overall accuracy value. Nevertheless, in terms of target-level accuracy using the default classification probability threshold (i.e., 0.5), Bootstrap Forests performed best with a classification accuracy rate of 50.4% at the target level. We refer to this Bootstrap Model as Model II.

By applying such a model, the direct selling company will have a 3.66 times greater probability of predicting candidates at the desired level than if there were no model.

To interpret these numbers, assume that a DSO uses this model to estimate the top 20% of existing representatives anticipated to net more than $10,000 annually through direct selling. In this situation, the company will have a 3.66 times greater probability of predicting candidates at the desired level than if there were no model.

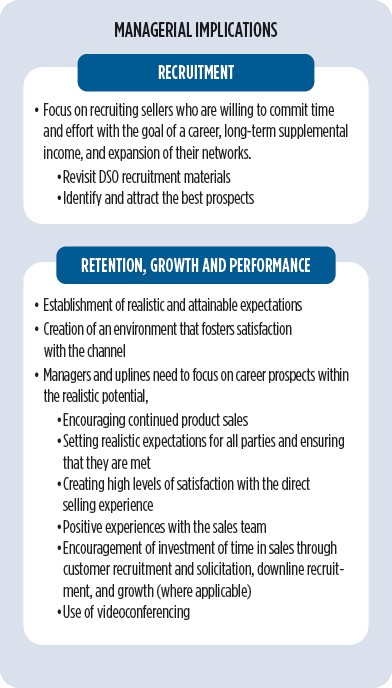

Recruitment

Using individual data that DSOs may secure before and at recruitment, Predictive Model-I can generate the probability that a new candidate is a preferred prospect because they are appropriate to the target audience of direct sellers who can generate more than $10,000 net annual income from a direct selling business.

Deploying the predictive Model I on a new population can correctly classify almost 78% of candidates to generate a $10,000 annual net income from direct selling. DSOs can apply such a model to identify and recruit the most productive candidates. Even though 88.3% of representatives are part-time, the top performers are interested in devoting their sales time and view direct selling as a career. While only 11% of direct sellers are male, they are more likely to become top performers (34% versus 15%).

We show that if a direct selling company uses Predictive Model I to select the top 20% of new representatives who are predicted to be most likely to generate more than $10,000 annual net income, the company will get 2.5 times more productive candidates than “no model baseline.” Here, no model baseline classifies everybody as belonging to the majority class (e.g., not likely to make more than $10K) in the historical data. While DSOs do not screen recruits, they could use this data to determine the best prospects and design recruitment materials, campaigns, and support systems to optimize performance, as well as creating adaptive learning systems to support incoming recruit success.

If a direct selling company uses Predictive Model I to select the top 20% of new representatives who are predicted to be most likely to generate more than $10,000 annual net income, the company will get 2.5 times more productive candidates than “no model baseline.”

Retention, Growth, and Performance

By using determinants available only after the recruitment of an independent representative, we calculated the likelihood of financial success in Predictive Model II.

This can assist companies to focus on factors that most significantly contribute to the financial success of direct selling representatives to lead to increased company growth and performance. By using a Bootstrap Forest technique, we show that Predictive Model-II can correctly classify 84% of representatives who are more likely to generate more than $10,000 a year. DSOs can develop organizational training and support based on this knowledge.

Predictive Model-II can correctly classify 84% of representatives who are more likely to generate more than $10,000 a year.

Study outcomes suggest DSOs prioritize recruiting sellers dedicated to building careers (business builders), earning long-term income, and expanding networks. This involves revamping recruitment materials to attract high-quality prospects instead of a broad range of recruits. This approach aims to reduce turnover and resources spent. While ensuring inclusivity, incorporating more male and Latinx representation may enhance sales performance.

DSOs are responsible for retaining and growing their representatives. They must set realistic expectations, create a satisfying environment, encourage product sales, and foster positive experiences within the sales team. Managers should focus on career prospects, recruit customers, grow downlines, and use videoconferencing.

DSOs differ in business models, size, reach, customers, products, missions, and cultures. They can benefit from firm-level predictive analytics and channel-level data insights. However, they should consider the research limitations and improve them with advanced methods.

Dr. Caroline Glackin is the Thomas Family Distinguished Professor of Entrepreneurship at the University of North Carolina Pembroke.

Dr. Murat Adivar is a Professor of Management at Fayetteville State University

By Suzanne Altobello, PhD, Caroline Glackin, PhD, and William G. Collier, PhD

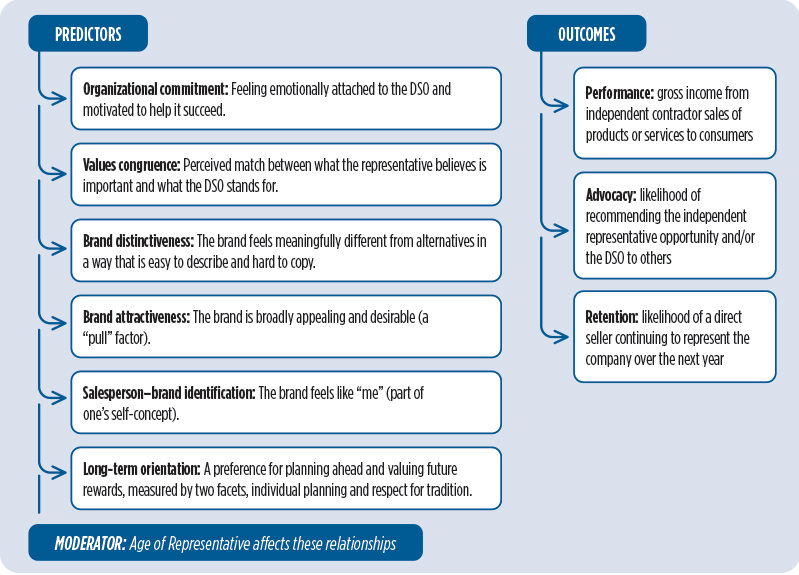

Direct selling depends on independent representatives who choose to stay, advocate for the opportunity, and help grow the salesforce. Because representatives are not traditional employees, direct selling organizations (DSOs) often win or lose on perceived fit and meaning between the representative and the company, rather than formal supervision. We examined whether identity-related perceptions, such as commitment, shared values, identification, brand meaning and long-term orientation, help to explain three practical outcomes of income, willingness to recommend the DSO/direct selling to others, and likelihood of continuing as a representative.

This research explores how independent sales representatives integrate into the brand and company, and how to strengthen these relationships. Previous studies in the sales literature have examined salesperson/brand identification with the organization and the congruence between personal values and perceived values of the organization, but have not addressed these factors for contract salespeople. This survey was designed for replication and extension of Gammoh et al. (2014) and engaged direct sellers from two organizations.

We modeled three outcomes that matter to DSOs: gross income from sales of products or services by their independent salesforce to consumers (performance), a direct seller’s likelihood of recommending the opportunity to one’s network (advocacy), and a direct seller’s likelihood of continuing to represent the company over the next year (retention). We tested whether these outcomes were predicted by Social Identity Theory constructs including: organizational commitment, salesperson–DSO values congruence, brand distinctiveness, brand attractiveness, salesperson–brand identification, along with long-term orientation (individual planning; respect for tradition). Figure 1 provides brief definitions of our predictors and outcomes.

Figure 1

Predictors and Outcomes in Research Models

Social Identity Theory

In practical terms, Social Identity Theory (SIT) helps explain why people work harder and stay longer when they feel they truly belong to a group or organization. Originating in social psychology, SIT argues that individuals define part of who they are through their membership in social groups, such as a company, a brand community, or a sales team (Fiske and Taylor, 1991; Tajfel, 1978; Tajfel and Turner, 1986; Ashforth and Mael, 2024). People tend to see their own group (the ingroup) more positively than other groups (outgroups) (Tajfel et al., 1971). When they believe their group has distinctive and attractive qualities, that pride in membership can boost self esteem and strengthen their desire to stay connected to the group (Fiske and Taylor, 1991). In sales and service settings, this logic underpins related ideas such as organizational identity (Karanika-Murray et al., 2015), moral identity (Itani and Chaker, 2022), perceived inclusion (Chen and Tang, 2018), salesperson brand identification, and salesperson company identification (Gammoh et al., 2014). All of these constructs capture how strongly people feel that “this organization or brand is part of who I am.”

For practitioners, the implication is straightforward: when representatives feel that “this company stands for what I stand for” and “this brand fits who I am,” they are more likely to stay, to advocate for the organization, and to deliver better performance.

Gammoh et al. (2014) and van Dick (2001) describe social identity as having cognitive, evaluative, emotional, and behavioral components. Cognitively, individuals see themselves as part of the group. Evaluatively and emotionally, they feel pride and positive regard for that membership. Behaviorally, they support the ingroup through actions that help and benefit it, such as going the extra mile for customers or defending the brand when it is criticized.

Gammoh et al. (2014) applied SIT to company employed salespeople and showed how these ideas translate into day-to-day performance. They found that when salespeople perceived strong value congruence (e.g., when their personal values matched the values of the brand and the company), they reported higher identification with both. This stronger sense of identity was linked to greater job satisfaction and organizational commitment. In turn, these attitudes were associated with more effective behavioral and outcome performance, including clearer communication and stronger sales results. For practitioners, the implication is straightforward: when representatives feel that “this company stands for what I stand for” and “this brand fits who I am,” they are more likely to stay, to advocate for the organization, and to deliver better performance.

Long-Term Orientation

Long-term orientation in selling captures whether a salesperson is focused on near-term transactions or on the future consequences of today’s behaviors for customer relationships and business outcomes. In sales settings, research suggests that a stronger consideration of future sales consequences, paired with customer-oriented selling, helps explain a salesperson’s long-term relationship orientation and related preferences such as favoring longer-term compensation approaches (Schultz & Good, 2000). Work on salespeople’s “relational time perspective” similarly argues that representatives with longer time horizons tend to set goals differently and rely more on cooperative, problem-solving approaches that support relationship development over time (Macintosh, 2006). More recent sales research also connects salesperson time orientation to outcomes such as sustained effort during a new product launch and customers’ willingness to pay more, highlighting that future-focused selling can matter for both salesperson behavior and customer responses (Agnihotri et al., 2019; Beuk et al., 2014).

Age as a moderator

For direct selling organizations, age is more than a demographic label; it can shape how representatives think about their role, how they relate to the company, and how they behave toward others. DSOs routinely attract people at very different stages of life, from young adults looking for a side income to older adults seeking flexible work in semi-retirement. Although research on how Social Identity Theory operates by age is still limited, several studies suggest meaningful age differences in the behavior component. Matsumoto et al. (2016) find that older individuals tend to engage in more prosocial behaviors, while Lockwood et al. (2021) report that adults aged 55 to 84 are more willing to help others than adults aged 18 to 36. Cutler et al. (2021) show that older adults are especially likely to direct prosocial behaviors toward people they see as members of their own group. In sales contexts, Day (1993) also finds that older salespeople set higher annual sales goals and achieve them just as well as younger colleagues. For DSOs, recognizing these age-related patterns can support more precise recruitment messages and motivational strategies that align with representatives’ life stage and long-term orientation, rather than using a single approach for all age groups.

A quantitative survey was sent via email to independent representatives of two established member companies of the Direct Selling Association. Both companies were similar in product characteristics but differed in overall revenues. All participant responses were anonymous and went directly to the research team. Companies did not have access to any raw, individual-level data.

Measures

The dependent variables in the analysis are each respondent’s gross income from direct selling in the previous year, the likelihood of recommending becoming an independent sales representative to a friend or family member, and the likelihood of continuing to represent the company over the next year. The independent predictor variables included: salesperson/company identification, salesperson/company values congruence, salesperson/brand identification, brand distinctiveness, brand attractiveness, organizational commitment, and long-term orientation. All SIT predictors were measured using established scales from Gammoh et al. (2014). Long-term orientation was measured using the Bearden et al. (2006) scale, which operationalizes long-term orientation at the individual level as two related factors: planning and tradition.

Sample profile

A total of 592 representatives started the survey; 295 respondents had complete data across all predictor and outcome measures. The ages of all current independent sales representatives ranged from 18 to 74, with a mean of 45.81 (SD = 11.24) years, with no significant differences in age between the companies.

Most respondents were between 40 and 50 years old (39.5%) and female (88.3%).

Almost 70% are married, with approximately equal percentages of single (8.2%) and divorced/separated (9.5%) respondents. Most representatives had no children under 18 at home (40.8%), with equal percentages having one (17.4%) or two children (20.8%). Most respondents were not of Hispanic or Latino origin (84.8%) and had attained an associate’s degree or some college (29.9%) or were college graduates (30.6%).

We first estimated separate stepwise regression models for each of the three outcomes.

We used all respondents in these initial analyses and did not separate by age group.

For sales performance (as measured by the respondent’s reported gross income from direct selling), organizational commitment was the only predictor that showed a statistically significant relationship. Representatives who reported higher organizational commitment also tended to report higher gross income from direct selling. None of the other predictors added meaningful explanatory power once commitment was taken into account.

For the advocacy outcome (as measured by the likelihood of recommending the DSO), organizational commitment and salesperson/company values congruence were the only significant predictors. Representatives who felt more committed to the organization and who perceived a stronger match between their personal values and the DSO’s values reported a higher likelihood of recommending the opportunity to others.

For the retention outcome (as measured by the likelihood of continuing as a representative over the next year), salesperson/company values congruence and brand distinctiveness emerged as significant predictors. Representatives who saw a stronger match between their own values and the values of the DSO, and who viewed the brand as meaningfully different from alternatives, were more likely to say that they intended to continue representing the company.

Table 1

Significant Predictors of Direct Selling Outcomes for all Representatives

| Outcome | Model Fit | Significant Predictors | β | t | Sig. |

| Performance | R2 = .018, F (1, 282) = 5.114, p < .025 | Organizational Commitment |

.133 | 2.261 | .024 |

| Advocacy | R2 = .344, F (2, 281) = 73.69, p < .001 | Organizational Commitment |

.405 | 6.597 | <.001 |

| Salesperson/DSO Values Congruence | .242 | 3.935 | <.001 | ||

| Retention | R2 = .325, F (2, 281) = 40.858, p < .001 | Salesperson/DSO Values Congruence | .378 | 6.195 | <.001 |

| Brand Distinctiveness | .153 | 2.500 | .013 | ||

Age as a Moderator

We then examined whether the patterns just described varied by age group.

Respondents were grouped into three categories: under 40, 40 to 50, and 51 and older, and the regression models were re-estimated within each group. For performance, no variables remained significant once the sample was split by age, so age related differences in income are not interpreted further.

For the likelihood of recommending the DSO, the predictors differed by age group.

Among representatives under 40, those who saw the brand as attractive and who felt strongly committed to the organization were more likely to say they would recommend the opportunity. For representatives aged 40 to 50, recommendation was highest when three elements coincided: they felt that their personal values matched the DSO’s values, they viewed the brand as attractive, and they reported strong organizational commitment. Among representatives 51 and older, a different pattern emerged. In this group, advocacy was higher when they perceived a strong values be match with the DSO, saw the brand as clearly distinctive from others in the market, and the sales rep had a stronger long-term, tradition-oriented outlook. At the same time, those over 50 who perceived the brand as highly attractive were actually less likely to recommend it.

Table 2

Positive and Negative Patterns of Predictors for Advocacy Outcome by Age Groups

| Predictor | Under 40 | 40–50 | 51+ |

| Organizational commitment | + | + | |

| Salesperson–DSO values congruence | + | + | |

| Brand attractiveness | + | + | – |

| Brand distinctiveness | + | ||

| Long-term orientation: respect for tradition | + | ||

| Long-term orientation: individual planning | |||

| Salesperson–brand identification |

For the likelihood of continuing with the DSO, a similar pattern of age specific drivers emerged, as shown in Table 3. Among representatives under 40, salesperson or DSO value congruence and brand attractiveness were significant positive predictors of continuation intentions. In the 40 to 50 group, brand attractiveness and the long-term orientation dimension capturing individual planning were significant and positive. Retention again looked different for the oldest group of representatives (51+). For older representatives, a strong values match and a clear sense that the brand is unique went together with stronger continuation intentions.

However, in this same age group, those who said that the brand felt very much like “me” and those who saw the brand as very attractive were less likely to say they planned to continue.

Table 3

Positive and Negative Patterns of Predictors for Retention Outcome by Age Groups

| Predictor | Under 40 | 40–50 | 51+ |

| Salesperson–DSO values congruence | + | + | |

| Brand attractiveness | + | + | – |

| Brand distinctiveness | + | ||

| Salesperson–brand identification | – | ||

| Long-term orientation: individual planning | + | ||

| Long-term orientation: respect for tradition | |||

| Organizational commitment |

For performance, organizational commitment was the only consistent driver in the full sample. When the sample was split into age groups, the income patterns were less stable and did not yield clear age-specific drivers. For independent sales representatives in this dataset, sales performance is tied most closely to whether representatives felt a durable bond with the organization.

For the advocacy outcome, across the full sample, recommending the DSO was higher if representatives were committed to the organization and their sense that the DSO’s values matched their own. When we examined advocacy by age groups, organizational commitment mattered for younger and midlife representatives, and values congruence mattered strongly for older representatives (notably, though, brand attractiveness moved in the opposite direction for this group).

For the retention outcome, for all representatives, the strongest pattern for continuing with the DSO was a values match with the DSO plus a belief that the brand is meaningfully distinctive. When separated by age, values congruence remained important for the youngest and oldest groups, while brand attractiveness mattered for the younger and midlife groups. The older representatives in this sample appeared less likely to continue when the brand felt highly attractive or when the representative reported that the brand felt very much like “me.”

Our results can be applied to existing independent sales representatives and extend to recruitment and onboarding new representatives. The DSO should begin with a shared core that strengthens organizational commitment and clarifies the organization’s values in observable, day-to-day terms; these two levers showed up repeatedly across this study’s three outcomes, and they are also the easiest to standardize across the salesforce.

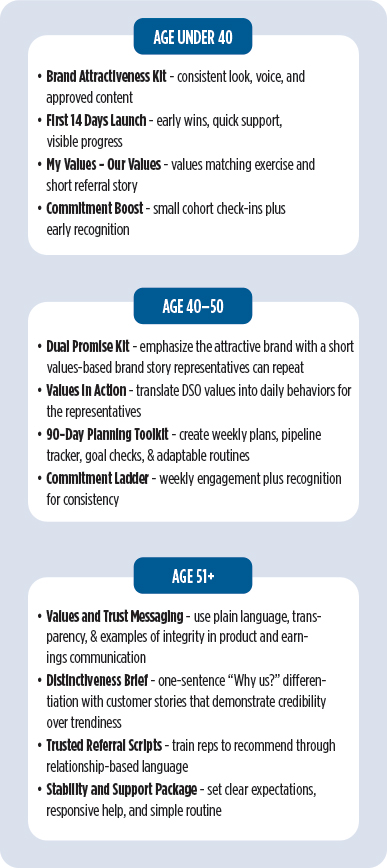

In Figure 2, we illustrate how the DSO can layer age-guided emphasis without changing the company’s fundamentals. Under 40 messaging and training could lean more heavily on brand attractiveness while quickly converting interest into commitment through early wins for the sales representative, belonging cues, and visible support through their upline. For ages 40–50, training might intentionally combine values fit, attractiveness, and commitment, then reinforce consistency through planning routines that keep the opportunity feasible alongside work and family obligations. For 51 and older, the emphasis could shift toward values congruence and brand distinctiveness, using concrete proof points and a trust-forward message; in this group, leaders should be careful about overreliance on hype or purely aspirational branding because it can work against advocacy and retention.

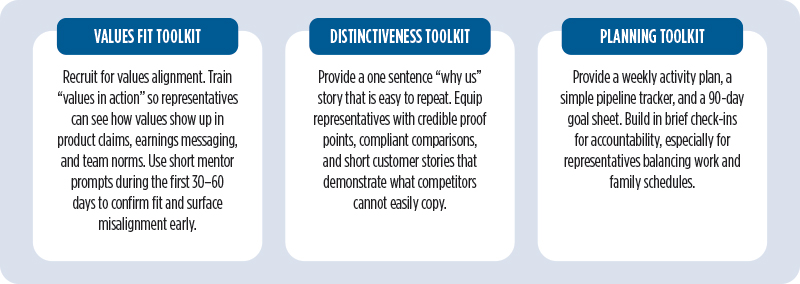

In Figure 3, we propose an overall toolkit architecture that DSO managers and leaders can use in coaching, communications, and recognition. The first toolkit could be a values fit toolkit that includes brief screening prompts during recruiting, a “values in action” onboarding module that shows how values appear in product claims and team norms, and mentor check-ins that surface misalignment early. The second toolkit could be a distinctiveness toolkit that gives representatives a one-sentence “why us” statement, compliant comparisons, and customer stories that make the brand’s difference easy to explain and hard to copy. The third toolkit could be a planning toolkit that provides weekly activity plans, 90-day goals, and pipeline tracking, especially for the 40–50 segment where planning aligned with continuation.

Dr. Suzanne Altobello is the William H. Belk Distinguished Chair of Business Administration and Professor of Marketing at University of North Carolina Pembroke.

Dr. Caroline Glackin is the Thomas Family Distinguished Professor of Entrepreneurship at the University of North Carolina Pembroke.

Dr. William Collier is an Associate Professor of Cognitive Psychology at the University of North Carolina Pembroke.

By Robert A. Peterson, PhD

Direct selling is a business model that offers entrepreneurial opportunities to individuals who, as independent contractors, market products and services to consumers, typically outside of a fixed retail establishment through one-to-one selling, in-home product demonstrations, or online. Direct sellers have job titles such as distributor, representative, consultant, associate, or brand partner. They may participate in direct selling in various ways, including selling products and services themselves or through their sales organizations, providing training and leadership to their sales organizations, referring customers to their company, and purchasing products and services for personal use. Compensation is ultimately based on sales and may be earned through personal sales and/or the sales of others in their sales organization.

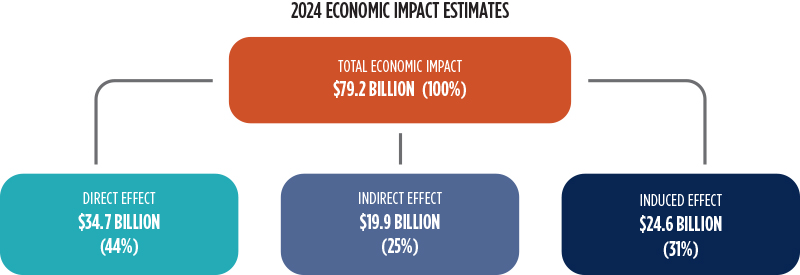

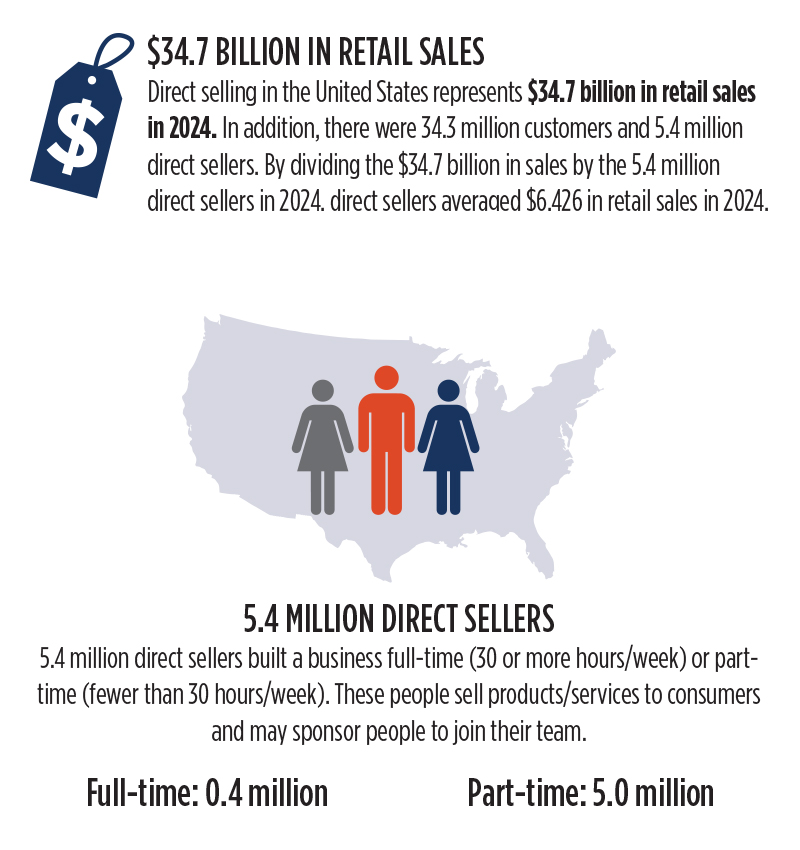

In 2024, direct selling generated $34.7 billion in retail sales in the United States and involved an estimated 5.4 million individuals who were actively engaged in building their own direct selling businesses.

Despite its ubiquity and contribution to the economy, the full economic impact of direct selling in the United States is often understated. Therefore, the purpose of the present analysis was to estimate the economic impact of direct selling activity in 2024 through the application of an input-output economic model. Given the retail sales generated by direct selling (i.e., its Direct Effect), the model (implemented by means of IMPLAN® software and data) estimated the

Collectively, these three effects—Direct, Indirect, and Induced—represent the economic impact of direct selling activity on the nation’s economy. In addition, the analysis estimated the fiscal (tax) implications of direct selling activity in the United States.

An input-output economic modeling of 2024 direct selling sales activity was undertaken using IMPLAN® software and data obtained from the federal government[1]. Direct selling (retail) sales data were provided by the Direct Selling Education Foundation (DSEF). The purpose of the modeling was to estimate the economic impact of direct selling activity in the United States in 2024.

Results are reported in terms of Direct, Indirect, and Induced Effects using a measure of gross economic output, sales dollars. Gross economic output refers to the cumulative value of production. Unlike Gross Domestic Product (GDP), gross economic output includes intermediate goods and services. (GDP is synonymous with total output less intermediate inputs.)

Using the DSEF estimate of $34.7 billion in direct selling (retail) sales in 2024 as a starting point, the total economic impact of direct selling activity in the United States in 2024 was estimated to be $79.2 billion. The $79.2 billion economic impact consisted of

Because of (1) the modeling approach and (2) the nature of the industry (e.g., the widespread use of independent contractors), the total estimated economic impact of $79.2 billion should be considered conservative.

The derived multiplier emanating from IMPLAN® modeling was 2.28. This multiplier means that nationally $1.00 in direct selling (retail) sales produced an economic impact of $2.28 in 2024.

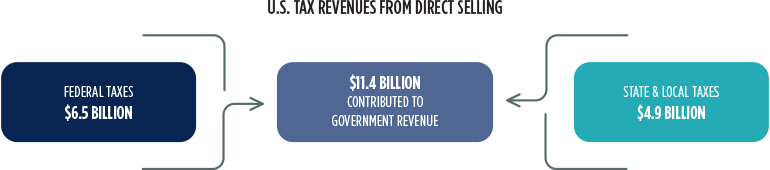

In 2024, the economic impact of direct selling activity produced an estimated $6.5 billion in federal taxes and $4.9 billion in state and local taxes, or $11.4 billion in total taxes. The total value of direct selling activity (i.e., the Direct, Indirect, and Induced Effects) added to the nation’s Gross Domestic Product in 2024 was estimated to be $79.2 billion.

The present modeling estimated the economic impact of direct selling activity in the United States in 2024 using the IMPLAN® input-output economic model. Specifically, in the present context, gross economic activity refers to sales dollars generated and distributed throughout the United States economy. The sources of activities that sum to economic output consist of both capital expenditures and operating expenditures, including spending on goods and services by direct selling firms, the Direct Effect, as well as by firms within the direct selling supply chain, which leads to the Indirect Effect, and off-site spending on goods and services by households in which a member earns income from a direct selling company or supply chain company, the Induced Effect.

A series of multipliers link Direct, Indirect, and Induced Effects. These multipliers are based on data compiled by several federal entities and include the Bureau of Economic Analysis Benchmark Input-Output Tables. (See Appendix for details.) A summary metric, the derived or implied direct selling multiplier, estimates the impact of one direct selling sales (retail) dollar on gross economic output due to inter-industry and industry-employee household relationships between the direct selling industry and other industries.

Conceptually, the multipliers quantify the economic ripple effect of inter-industry economic activity. This ripple effect can be positive or negative depending on whether a modeled entity is expanding or contracting. Multipliers are static and do not account for disruptive shifts in infrastructure without specifically addressing infrastructure changes. The present model applies the most current (2024) IMPLAN® multipliers.

Data

DSEF conducts an annual “Growth & Outlook” market-sizing survey to estimate the size and scope of the direct selling industry in the United States. It engages Cadmus, an international consulting firm, to conduct this survey, perform secondary research, and generate industry-wide estimates.

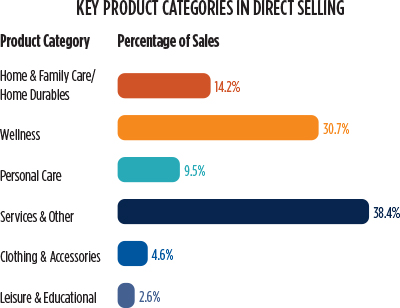

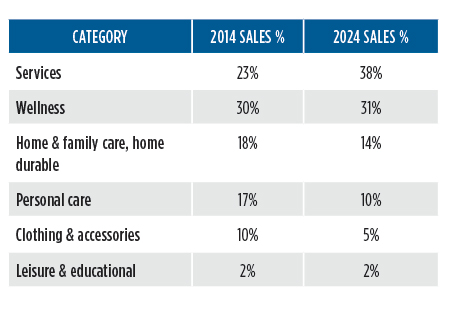

Cadmus market-sizing estimates are reviewed and further refined by DSEF. Results that are reported include total direct selling (retail) sales as well as (retail) sales estimates by selected geographical regions, by compensation structure of direct selling firms, by sales strategy, and by major product categories. The six product categories utilized in the present analysis are:[2]

The DSEF’s 2025 Growth & Outlook Report (retail) sales estimate formed the basis of IMPLAN® modeling. Specifically, according to the DSEF, direct selling (retail) sales totaled $34.7 billion in 2024. The $34.7 billion in direct selling (retail) sales was initially modeled in IMPLAN® with margins applied. This was equivalent to identifying the economic impact of operating a business with $34.7 billion in retail sales. It excluded the manufacturing, wholesaling, and transporting of goods, and included only the economic activities associated with direct selling companies.

Wholesaling and manufacturing Indirect Effects of direct selling activity due to the industry supply chain were sequentially modeled by respectively applying margins to direct selling (retail) sales activity and wholesale sales activity. For wholesaling, this allowed the identification of the economic effects of operating the equivalent of a wholesale business. The wholesale industry modeling included transportation but excluded the effect and supply chain of the manufacturing component.

Manufacturing activity was estimated after applying margins to and subtracting direct selling economic activity and wholesaling economic activity. Manufacturing sales activity was modeled using the six product groups (e.g., wellness, personal care, etc.) above.

The Induced Effect of direct selling activity was estimated for each sector modeled (i.e., retailing, wholesaling, and manufacturing) and aggregated to reflect its total estimated economic impact.

Taxes attributable to direct selling activity were also estimated using the IMPLAN® model. The tax estimates provided in this report include tax revenue derived from direct, indirect, and induced sales activity. The national economic impact tax estimate includes both federal taxes and state/local taxes.

The $34.7 billion in direct selling (retail) sales nationally contributed a total economic impact of $79.2 billion to the national economy in 2024 through its combined indirect and induced effects. As shown above, the 2024 national economic impact included $34.7 billion in direct selling sales activity, $19.9 billion in indirect sales activity, and $24.6 billion in induced sales activity.

The derived (implied) multiplier resulting from IMPLAN® modeling summarizes the economic impact of one direct selling (retail) sales dollar ($1) on the national economy. It is calculated as the total economic impact divided by the direct effect (i.e., $79.2B/$34.7B = 2.28 in 2024). Thus, for example, $1 in direct selling sales (the direct effect) generated a total economic impact of $2.28 in 2024. The derived multiplier in 2024 is somewhat smaller than derived multipliers observed in other retailing sectors (approximately 2.44 on average).

Tax impacts estimated by IMPLAN® are respectively categorized as federal taxes and state and local taxes. IMPLAN® quantifies tax impacts based on employee compensation, proprietor income, and taxes on production and imports, households, and corporations. Estimated taxes range from federal and state income taxes and property taxes to sales taxes and motor vehicle licenses. As such, the estimated total (direct, indirect, and induced) federal, state, and local tax revenues attributable to direct selling activity in the United States in 2024 were $11.4 billion. Federal tax revenues attributable to the $34.7 billion in direct selling activity were estimated at $6.5 billion in 2024. State and local taxes attributable to direct selling activity were estimated at $4.9 billion in 2024.

IMPLAN® is an input-output economic model based on aggregating and connecting a multitude of economic databases, foremost of which are the Bureau of Economic Analysis (United States Department of Commerce) Benchmark Input-Output Tables.[3] It consists of both software and data that together permit detailed estimates of various economic impacts. The IMPLAN® model quantifies inter-industry relationships within an economy by documenting how the output of one industry becomes the input of another industry. Through a backward-linking process, the present modeling captured the relationship between economic activity in the direct selling industry and economic activity in its (general) supply chain (i.e., the Indirect Effect of direct selling activity on the wholesaling and manufacturing firms in the direct selling industry supply chain) as well as the ancillary (household) effect that direct selling activity has on the economy (i.e., the Induced Effect).

The primary databases contained and used in IMPLAN® modeling are respectively compiled and updated by the United States Census Bureau, the United States Bureau of Economic Analysis, the United States Department of Agriculture, and the United States Bureau of Labor Statistics.

Numerous multipliers were used in the present analysis to link the six (aggregated) product categories and the manufacturing sector (which were in turn linked to the wholesale and retail sectors). In particular, product subcategories were matched with 6-digit NAICS codes which were in turn linked to their respective 528 IMPLAN® sectors. Because the Nonstore Retailers Sector encompasses more establishments than those traditionally defined as direct selling companies, its associated multiplier might be somewhat attenuated. However, any possible attenuation was not believed to substantially affect the results of the estimation process or the final economic impact estimation due to limiting the modeling to particular product categories.

Specifically, when modeling the manufacturing sector, the multipliers associated with the six direct selling product categories incorporated the categories’ relative sales and the percentage of category manufacturer sales that originated in the United States (based on federal data sources). The 2024 direct selling (retail) sales percentages were based on the DSEF’s 2025 Growth & Outlook Report estimates, whereas the 2024 domestic purchasing percentages (related to local purchasing coefficients in IMPLAN®) were based on 2023 federal statistics.

Within the six product categories, subcategories were aggregated to form each respective product category. For instance, as previously shown, two IMPLAN® subcategories (Clothing, Lingerie, Sleepwear and Shoes, and Jewelry and Fashion Accessories) were aggregated to create the Clothing & Accessories product category. Trade flows and industry data for the subcategories were combined in IMPLAN®, and multipliers were generated by IMPLAN® software. (Note: the combination was not a simple average.) To the extent that product category data do not comport exactly with direct selling product offerings or sales, the multipliers might be somewhat attenuated. However, the consequence of such potential attenuation was not deemed substantial.

The overall derived multiplier, 2.28, was composed of the Direct Effect implied multiplier 1.00, the Indirect Effect implied multiplier .57, and the Induced Effect implied multiplier .71.

Where appropriate, default values of the IMPLAN® software were applied during modeling. Consequently, all estimated values—multipliers as well as effects and impacts—should be considered conservative.

[1] IMPLAN® is widely used in industry and government analyses. See www.implan.com

[2] The product categories include, but are not limited to, the illustrative subcategories.

[3] Frances Day, “Principles of Impact Analysis & IMPLAN® Applications.” IMPLAN® stands for IMpact Analysis for PLANning.

Dr. Robert Peterson is Professor Emeritus of Marketing and John T. Stuart III Centennial Chair of Marketing (Emeritus) at The University of Texas.

Appreciation is expressed to the Business Research Division, Leeds School of Business, University of Colorado, Boulder, for its analytical support.

By Monica Wood

Direct selling is a go-to-market strategy that is an alternative channel to retail. Individual independent distributors market and sell products and services to consumers in direct selling. The channel allows companies to reach customers through personalized interactions rather than relying on traditional storefronts. It also offers distributors flexible earning opportunities by building relationships and leveraging word-of-mouth marketing.

Some of the world’s most storied companies and recognizable brands market today’s leading-edge products through the direct selling channel – these include jewelry, cookware, nutritionals, cosmetics, housewares, energy, insurance, and much more. By leveraging direct selling, these companies create a more personalized customer experience that highlights product benefits in real-world settings. This approach also allows brands to expand their reach through trusted relationships and community-based engagement rather than traditional retail environments.

The direct selling channel differs from broader retail in how it gets great products and services into the hands of consumers. It’s an avenue where entrepreneurial-minded Americans can represent the products they love, while they work independently to build a business on their own terms. This personalized model allows consumers to engage with products through trusted, one-on-one interactions that traditional retail rarely provides. It also empowers individuals to turn their passion into income by building customer relationships and growing their business at their own pace.

Consultants forge strong personal relationships with prospective customers, primarily through face-to-face discussions and demonstrations. In this age of social networking, direct selling is a strategy that many marketers of consumer products find more effective than traditional channels. By combining personal interaction with digital outreach, consultants can create a seamless customer experience that builds trust and engagement. This hybrid approach allows brands to reach consumers where they are—both online and in their communities—while maintaining the authenticity and connection that drive purchasing decisions.

Millions of Americans from every state, congressional district and community in the United States choose direct selling because they enjoy a company’s products or services and want to purchase them at a discount. Some decide to market the products they love to friends, family, and others and earn commissions from their sales. The most successful consultants may decide to expand their businesses by building a network of direct sellers. This model allows individuals to grow at their own pace, whether they simply want to save money or aspire to build a business. As a result, direct selling attracts a broad mix of people who value flexibility, community, and the ability to shape their own economic futures.

Ninety-two and a half percent of direct sellers decide to work part-time, offering busy parents, caregivers, military spouses, veterans, and others flexibility and work-life balance. As advancements in technology create a new American economy whose foundation is built upon the entrepreneurial spirit and independent work, historically, direct selling has been one of the oldest ways millions of Americans have chosen to work independently—long before the advent of the Internet. Direct selling has a long history of substantially contributing to the economy and supporting the millions of Americans involved.

Its adaptability has enabled the direct selling channel to remain relevant through changing economic conditions, technological evolutions, and shifting consumer behaviors. This longstanding resilience underscores the sector’s role as a reliable pathway for individuals seeking autonomy and economic opportunity.

5.4 million direct sellers have built a full-time business (30 or more hours/week) or part-time (fewer than 30 hours/week) representing a correction after the hypergrowth of the pandemic. These people sell products/services to consumers and may sponsor people to join their team.

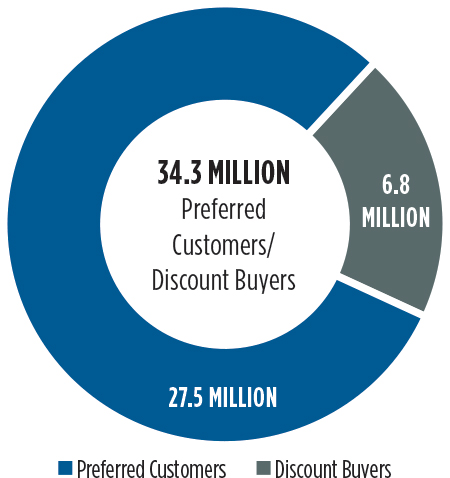

6.8 million Discount Buyers are eligible to purchase, sell and sponsor but currently only purchasing products and services they personally enjoy and receive at a discount.

27.5 million Preferred Customers have signed a preferred customer agreement with a direct selling company where they may be entitled to pay wholesale prices for products and services but are not eligible to sell.

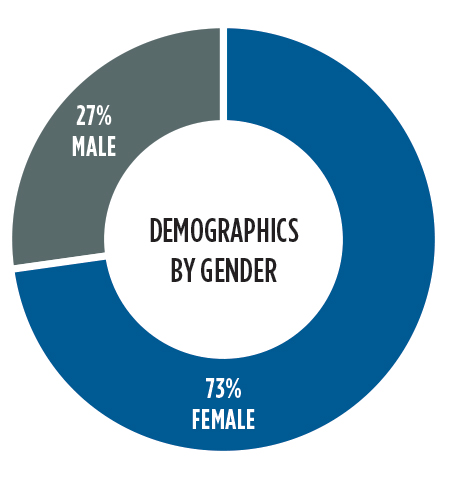

The demographic data show that the direct selling population is predominantly female, with women representing 73% of participants, and most individuals fall within the 35–54 age range. Participation spans all age groups, indicating that direct selling appeals to both younger adults seeking flexibility and older adults pursuing supplemental income.

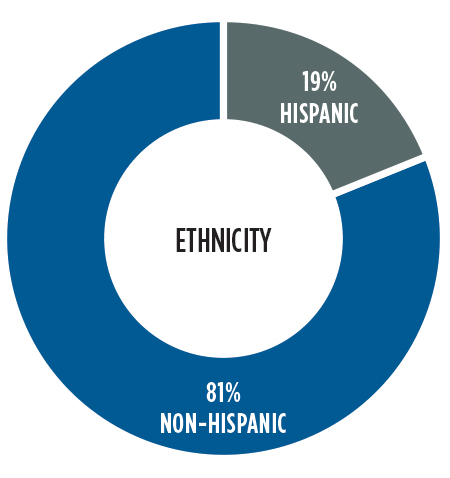

When considering direct seller ethnicity, 19% of participants identify as Hispanic, reflecting meaningful engagement from a key and growing demographic segment.

When considering direct seller ethnicity, 19% of participants identify as Hispanic, reflecting meaningful engagement from a key and growing demographic segment.

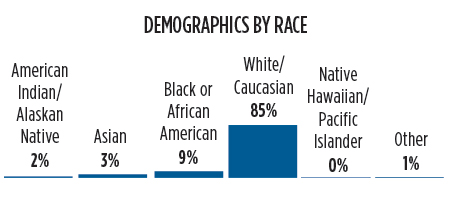

The 2025 Growth & Outlook survey results indicate that service-based offerings have experienced substantial growth and now represent the largest share of sales, highlighting strong consumer interest in digitally enabled and value-added services. Wellness products continue to maintain a significant portion of the market, demonstrating their enduring appeal. Meanwhile, the gradual shifts in product-oriented categories—such as personal care, home and family care, clothing, and leisure—represent opportunities for companies to innovate, reposition their portfolios, and meet emerging consumer preferences more effectively.

12.2 million people in the U.S. signed or renewed independent contractor sales agreements with direct selling companies in 2024. Of these 12.2 million, 5.4 million worked to build businesses and 6.8 million were discount buyers who purchased products for their own use but chose not to build a business. These estimated direct sales and people-involved figures are extrapolated based on 2025 Growth & Outlook Survey data submitted directly from DSA members.

| State/Territory | People Involved in Direct Selling | Retail Sales |

|---|---|---|

| Alabama | 120,971 | $446M |

| Alaska | 69,150 | $162M |

| Arizona | 231,808 | $620M |

| Arkansas | 116,320 | $362M |

| California | 1,285,088 | $3.9B |

| Colorado | 276,515 | $626M |

| Connecticut | 96,649 | $284M |

| Delaware | 35,730 | $127M |

| Florida | 827,479 | $2.2B |

| Georgia | 396,711 | $1.1B |

| Hawaii | 53,605 | $85M |

| Idaho | 103,444 | $246M |

| Illinois | 425,529 | $1.2B |

| Indiana | 309,809 | $857M |

| Iowa | 204,866 | $647M |

| Kansas | 133,993 | $353M |

| Kentucky | 142,370 | $404M |

| Louisiana | 134,146 | $465M |

| Maine | 64,641 | $187M |

| Maryland | 195,114 | $531M |

| Massachusetts | 140,495 | $434M |

| Michigan | 359,404 | $0.9B |

| Minnesota | 266,638 | $714M |

| Mississippi | 130,921 | $616M |

| Missouri | 194,361 | $492M |

| Montana | 68,031 | $160M |

| Nebraska | 117,414 | $344M |

| Nevada | 107,862 | $266M |

| New Hampshire | 84,186 | $226M |

| New Jersey | 257,016 | $762M |

| New Mexico | 81,552 | $213M |

| New York | 591,642 | $1.9B |

| North Carolina | 410,045 | $1.1B |

| North Dakota | 61,152 | $188M |

| Ohio | 416,559 | $1.0B |

| Oklahoma | 191,781 | $459M |

| Oregon | 142,972 | $418M |

| Pennsylvania | 395,806 | $1.0B |

| Rhode Island | 35,506 | $111M |

| South Carolina | 182,085 | $470M |

| South Dakota | 66,977 | $201M |

| Tennessee | 248,566 | $758M |

| Texas | 1,219,347 | $3.6B |

| Utah | 190,869 | $514M |

| Vermont | 19,937 | $72M |

| Virginia | 282,753 | $706M |

| Washington | 226,305 | $611M |

| West Virginia | 62,501 | $175M |

| Wisconsin | 278,227 | $816M |

| Wyoming | 39,040 | $90M |

| District of Columbia | 8,464 | $18M |

| Guam | 7,006 | $8M |

| Puerto Rico | 63,550 | $544M |

| U.S. Virgin Islands | 1,458 | $6M |

| N. Marian Islands | 14 | $15M |

| American Samoa | 171 | $0.2M |

| Overseas U.S. Military | 4,421 | $14M |

The direct selling channel remains a viable and strategically significant avenue for companies that prioritize innovation and align their offerings with contemporary consumer expectations. The increasing integration of artificial intelligence is improving the training, development, and empowerment of prospective sales representatives, thereby fostering heightened entrepreneurial engagement across the sector. The continued emphasis on product quality and meeting consumer needs is critical to establishing a strong foundation for sustainable growth. Additionally, as consumer preferences evolve in a dynamic marketplace, opportunities for long-term competitiveness within the direct selling landscape are likely to increase.

Entrepreneurial trends show an increase in participation in activities like direct selling, gig work, and online selling. The number of respondents working as direct sellers has tripled since 2008, with 1 in 3 expressing specific interest in the direct selling opportunity.

Key attributes that draw consumers to direct selling include the opportunity to support local businesses, access to distinctive products, and engagement with knowledgeable sellers. Social media continues to serve as an important mechanism for direct sellers to reach prospective customers, despite a decline in its perceived usefulness for maintaining connections and staying informed.

Overall, the study reflects a growing interest in flexible work arrangements, including direct selling. In an effort to enhance its appeal, the channel might consider further leveraging its strengths—such as personalized service, unique product offerings, and a strong sense of community.

Monica Wood is the Vice President of Consumer and Member Insights at Herbalife and Chair of the DSEF Industry Research Committee.

By Peter Marinello

For over a century, American businesses have embraced the belief that industries should be accountable for maintaining their own ethical standards. This principle is especially ingrained in the direct selling channel, where consumer trust and entrepreneurial opportunity have long gone hand in hand.

Since the 1970s, the Direct Selling Association (DSA) has upheld this commitment through a comprehensive Code of Ethics, overseen by an independent administrator, which governs everything from marketing practices to income disclosures.

Even before the rise of social media and digital advertising transformed the marketplace, DSA member companies recognized that trust is not imposed by regulation—it’s cultivated through consistent, principled behavior. Strengthening trust in the direct selling channel requires companies and their independent salesforce members to uphold ethical, transparent, and substantiated marketing practices.

Central to this effort is BBB National Programs’ Direct Selling Self-Regulatory Council (DSSRC), an independent oversight program created in 2019 in partnership with DSA. DSSRC offers a robust and technologically advanced self-regulatory model that builds on the channel’s existing business ethics foundation. Leveraging modern internet-wide monitoring tools, DSSRC reviews online direct-selling promotional content to identify potentially misleading product and income claims and engages with companies to resolve issues quickly before they escalate.

In an era where digital misinformation travels at lightning speed, the channel’s continued support for independent, proactive self-regulation is not only prudent—it is essential to preserving trust and credibility.

This article explores the value of industry-led self-regulation as a tool for promoting business accountability, protecting consumers, and strengthening public trust. In the direct selling sector, DSSRC exemplifies this commitment, working independently, but alongside companies, trade associations, and compliance professionals to up-hold ethical standards and proactively address emerging challenges. By complementing government oversight, self-regulatory initiatives like DSSRC demonstrate how independent monitoring and accountability can support sustainable business practices to reinforce confidence in the industry over the long term.

At BBB National Programs, industry self-regulation refers to a structured, voluntary process in which industries adopt and adhere to standards of conduct that promote responsible business practices, protect consumers, and address potentially deceptive or misleading behavior—often before regulatory action becomes necessary.

Effective self-regulation is rooted in independent oversight, transparent procedures, and a credible commitment to accountability. It empowers industries to lead in shaping ethical norms while building a culture of compliance.

Self-regulation initially emerged in the US as a proactive response to consumer protection challenges. In 1971, the National Advertising Division (NAD) was established by leaders in the advertising industry to set a new benchmark for independent review of truth-in-advertising claims. Administered by BBB National Programs, NAD has long served as a reliable and efficient forum for resolving advertising disputes and upholding standards of truth and accuracy—offering an alternative to the time and expense associated with litigation.

It is important to recognize that self-regulation is not a replacement for government enforcement. Rather, it acts as a complementary safeguard, offering a proactive approach that allows industries to identify and correct problematic practices early. Regulatory agencies such as the FTC have recognized the value of credible independent self-regulation, often referring matters to self-regulatory programs or factoring voluntary compliance into their enforcement decisions.

Self-regulation delivers substantial benefits to businesses, consumers, and regulators alike.

Ultimately, industry self-regulation—when done right—bridges the gap between the industry stakeholders and public accountability, reinforcing ethical standards that benefit the marketplace as a whole. By allowing businesses to reconcile misleading or unsubstantiated claims early, advertising self-regulation programs help prevent consumer harm, level the playing field for reputable business to engage with consumers and support the broader public interest.

Direct selling is a global method of marketing and retailing goods and services that takes place outside of a fixed retail location. It typically involves independent salesforce members—often referred to as distributors, consultants, or ambassadors —who engage in person-to-person sales, whether through in-home demonstrations, online platforms, or social networks. Beyond selling products, direct selling offers individuals the opportunity to build a business with low entry barriers, flexible hours, and the potential for supplemental income.

The industry operates at significant scale. According to the World Federation of Direct Selling Associations, the global direct selling market surpassed $167 billion in sales in recent years, with more than 100 million independent sellers participating worldwide. In the US alone, DSA reports that tens of millions of individuals are engaged in the channel.

The creation of DSSRC in 2019 was driven by the direct selling channel’s recognition of the need and desire to demonstrate continued commitment to ethical conduct and to modernize business compliance practices for companies across and outside of DSA membership. Rooted in the belief that integrity and responsible conduct drive sustainable growth, DSA and its member companies recognized the importance of enhancing consumer and regulatory trust through transparent, responsible business and marketing practices.

DSSRC was established as a proactive initiative to reinforce the industry’s values expressed in the DSA Code of Ethics and ensure that direct sellers’ product and income claims align with high standards of integrity and accountability— reinforcing the central role that trust and transparency play in the direct selling channel’s long-term success.

To create concrete impact, DSA partnered with BBB National Programs to create DSSRC as an independently administered self-regulatory program. Serving as an impartial monitor of the marketplace and independent of DSA, DSSRC reviews income and product claims made by companies and their independent salesforce members, addresses complaints, and refers matters to regulators when appropriate. This initiative provides a transparent and effective mechanism for accountability.

For self-regulation to be a meaningful force in promoting trust and integrity in the direct selling channel, it must be built on four foundational pillars: credibility, transparency, accountability, and an objective standard of review.

Credibility begins with independence. To be most effective, a self-regulatory program should be administered by a third party that is free from industry influence, ensuring that decisions are impartial and grounded in established principles rather than business interests. This independence lends weight to its findings and garners respect from both industry participants and regulators.

Transparency is often the most challenging and important component in establishing a credible self-regulatory framework. Processes must be clearly defined, publicly accessible, and include the publication of decisions or outcomes to demonstrate how standards are applied. This openness not only builds confidence among stakeholders but also serves as a guiding framework for industry-wide compliance. DSSRC maintains program transparency through publicly available case decisions, annual reports that highlight the basis for DSSRC’s findings and the companies’ responses and the publication of industry guidance.

Accountability ensures that businesses are held responsible for their conduct. A self-regulatory program must have effective mechanisms to address non-compliance and, when necessary, escalate unresolved matters to government agencies. Accountability is achieved by DSSRC through a structured referral system: when companies fail to respond, refuse to make the recommended changes, or cannot be located, DSSRC refers these matters to the FTC or the appropriate state attorney general.

Finally, an objective standard of review requires that all marketing claims, particularly those concerning income opportunities and product efficacy, are communicated truthfully and accurately and are substantiated by reliable evidence.

As Drs. Linda and O.C. Ferrell of Auburn University outline in their article featured in this journal, self-regulation allows industries to proactively establish standards, build public trust, and maintain credibility without relying solely on external enforcement. This principle is demonstrated across a range of sectors.

Through these efforts, businesses demonstrate that self-regulation is not only a tool for compliance but also a commitment to ethical leadership and public accountability.

DSSRC similarly exemplifies these principles through a rigorous and impartial process. DSSRC proactively monitors the marketplace, identifying potentially problematic claims across digital platforms, including social media and independent salesforce communications. These findings trigger formal inquiries in which DSSRC reviews the claim in the context of the advertising, engages with the company, and issues a public case decision with recommendations for corrective action, when necessary.

Since its inception, DSSRC has identified over one million pieces of online content across various platforms related to direct selling companies and their independent salesforce members. DSSRC inquiries have resulted in the removal or substantial revision of more than 4,000 product and earnings claims disseminated by almost 500 different direct selling companies, significantly reducing the presence of misleading or unsubstantiated information in the marketplace.

A recent study conducted by Dr. Sandy Jap of the Goizueta Business School at Emory University examining the effectiveness of DSSRC found that the self-regulation program provides substantial benefits to DSA-member companies. An article highlighting Dr. Jap’s findings is also featured in this journal. Compared to non-member organizations, DSA members exhibit stronger adherence to responsible marketing practices. Dr. Sandy Jap’s independent analysis of DSSRC case data shows that DSA members make fewer product and income claims, respond to compliance concerns more promptly, and are less likely to require additional enforcement to resolve violations.

The study also revealed that DSA members resolve inquiries more efficiently and show higher levels of cooperation with DSSRC’s final decisions. Moreover, DSA members are significantly more proactive in modifying or removing problematic claims and addressing compliance issues, distinguishing them from non-DSA member companies.

Credible self-regulation promotes a level playing field by holding companies to consistent standards, discouraging bad actors, and reinforcing the integrity of the broader industry. For responsible businesses, self-regulation is not a shield against external scrutiny—it’s a strategic commitment to long-term sustainability, transparency, and public confidence.

Building a Foundation for Responsible Business Practices

Sustaining consumer trust in the direct selling channel requires more than reactive enforcement—it demands a long-term commitment to transparency, ethics, and responsible business practices. Since 2019, DSSRC has played a pivotal role in helping the channel establish and uphold these principles. By working collaboratively with companies and offering guidance grounded in legal and regulatory expectations, DSSRC has helped shift the channel toward a more proactive and preventative compliance culture.

A key component of this shift has been DSSRC’s focus on education and outreach. Through webinars, guidance, one-on-one consultations, and published case decisions, DSSRC provides companies and their independent salesforces with practical tools to identify and avoid problematic claims.

A cornerstone of this effort has been the development of practical compliance guidance for direct selling companies and their salesforce. DSSRC collaborated with industry stakeholders to produce the Guidance on Earnings Claims in the Direct Selling Industry and the Guidance on Income Disclosure Statements in the Direct Selling Industry. These resources serve as clear, objective frameworks for ensuring that income-related representations are presented in a way that avoids ambiguous or unsupported projections of expected income for prospective salesforce members interested in the direct selling business opportunity.

Through company education, DSSRC has also contributed to the decline of outdated and potentially misleading terms, such as “financial freedom,” “unlimited income,” and “career-level income,” which were once common in the channel. Today, companies are more mindful of the language used in promotional materials, leading to improved claim substantiation and enhanced consumer protection, building a stronger foundation for ethical growth across the channel.

As the direct selling channel continues to evolve, so must the standards that govern it. Emerging challenges from digital marketing, social media, influencer promotion, and international expansion require adaptive oversight. DSSRC has expanded its monitoring scope to include influencer content, global claims, and even AI-generated promotional materials.

By embracing new technologies and staying ahead of marketplace trends, DSSRC ensures that self-regulation remains relevant, effective, and responsive—providing timely guidance that helps companies navigate complexity while upholding consumer trust and ethical standards in a rapidly shifting environment.

As policymakers consider the future of consumer protection in the direct selling channel, several core principles of effective self-regulation should be reinforced.

Conclusion

Robust, independent self-regulation is a powerful tool for reinforcing trust, credibility, and long-term success—particularly in dynamic distribution channels like direct selling. By taking ownership of high standards and ethical business practices, direct selling companies can demonstrate accountability, protect consumers, and elevate the reputation of the entire channel.

The work of DSSRC exemplifies how industry-led oversight—rooted in transparency, education, and proactive monitoring—can effectively reduce the need for reactive enforcement and align business practices with public expectations. As direct selling continues to evolve, sustained collaboration among industry leaders, regulators, and consumer advocates will be essential to strengthening marketplace trust.

Dr. Sandy Jap

The direct selling channel seems to be a favored target for Federal Trade Commission (FTC) scrutiny. In 2019, the Direct Selling Self-Regulatory Council (DSSRC) was established by the Direct Selling Association (DSA) in partnership with the BBB National Programs (BBBNP). The mission of the DSSRC is to enhance consumer and regulatory confidence in the advertising and marketing practices of the direct selling channel through independent, third-party review of claims disseminated by or on behalf of direct selling companies. Since its founding in 2019, the job of the DSSRC has been to educate and encourage direct selling companies to follow and comply with ethical sales and advertising practices.

Has this self-regulation effort in the direct selling channel been effective? Industry self-regulation is an important, yet under-studied phenomenon in business of which we know little. And whether self-regulatory organizations are truly successful at curbing marketing misbehavior is an open question that I seek to answer. To this end, we conducted an evaluation of the effectiveness of the DSSRC’s efforts and case outcomes since its inception in 2019 through February 2024. This analysis was based on their internal reports as well as those represented in the BBB and DSSRC database. Here is the evidence, by the numbers. For the full report, please click here.

Self-monitoring reduces inappropriate marketing practices. First and foremost, there is substantial support for the DSSRC’s value in promoting self-regulation and ethical sales and marketing practices in the direct selling channel. Over the five-year period, the DSSRC accomplished the following:

This leads to the conclusion that the DSSRC’s self-regulation efforts represented a substantial workload that did not land on the FTC’s desk, require an intervention by a state attorney general office or persist unaddressed.

DSA membership matters. DSA members showed clear evidence of better and more compliance with ethical marketing practices than non-DSA members. While the full report details a substantial number of statistically significant differences between the behaviors, claims and investigative outcomes of inquiries brought against DSA member companies and non-DSA member companies, I highlight a few here:

1) DSA member companies (compared to non-DSA member companies) have fewer product and earning inquiries than non-members. Moreover, their DSA member company consultants are more responsive at removing and modifying problematic product and income earning claims.